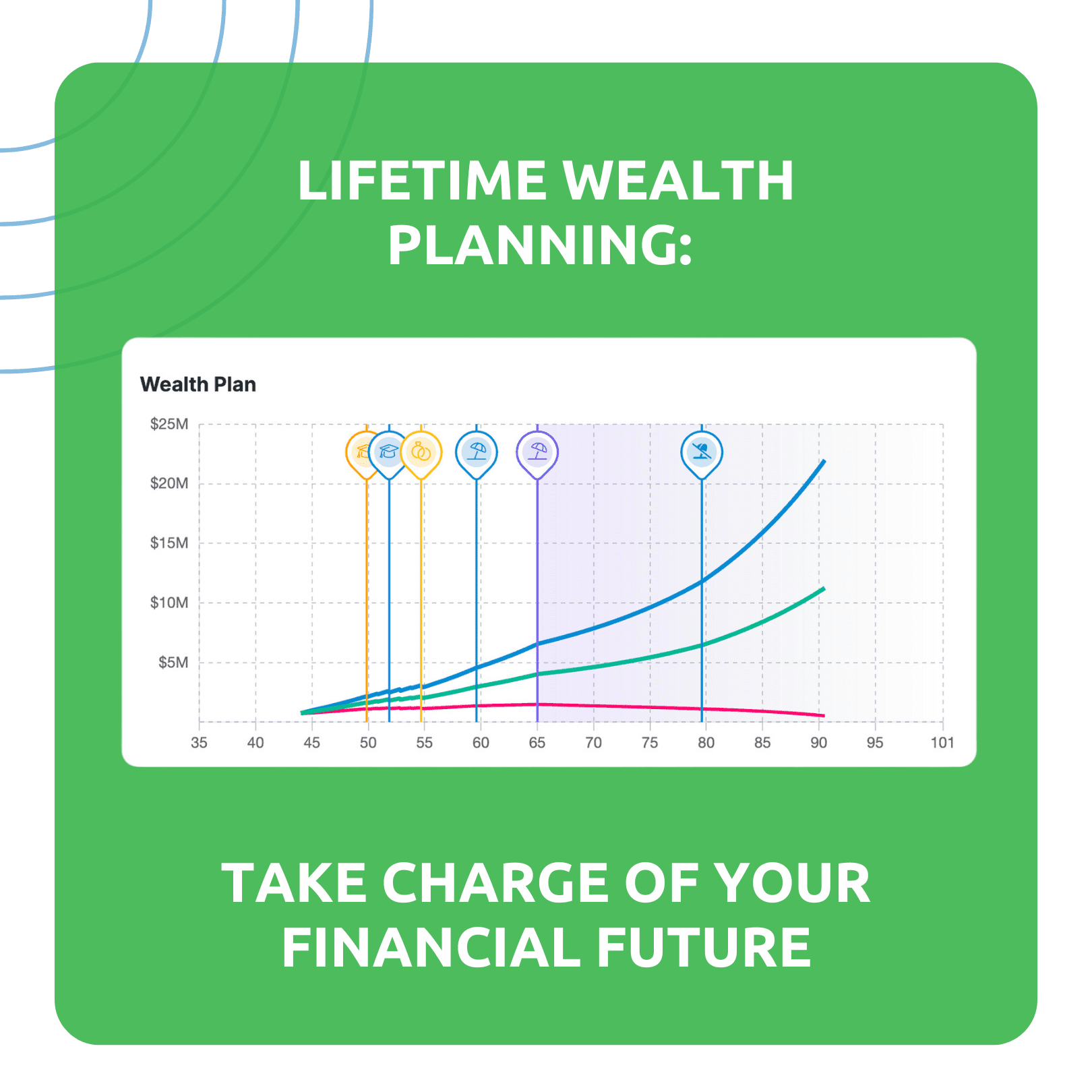

When we think about wealth, it’s not just about accumulating assets in the short term—it’s about building and protecting your financial future throughout your entire life. Lifetime wealth planning considers that your financial decisions today and tomorrow align with all your long-term goals, such as retirement, education costs, bequeathment, and major life events.

Unlike traditional financial planning, which might focus on one aspect of your finances at a time, WealthFluent lifetime wealth planning takes a holistic view. It integrates savings, investments, spending, borrowing, and risk management into one comprehensive approach that adapts as your life evolves.

Why Lifetime Wealth Planning Matters

For many people, financial planning is done in pieces. We might save for retirement through a 401(k) or IRA, buy a home with a mortgage, and invest in the stock market—all in separate decisions. However, these decisions can be inefficient or misaligned without a unified lifetime expected net wealth versus risk strategy. You may be saving for retirement without accounting for future expenses like your children’s education or investing aggressively when you should be preparing for a large purchase like a second home.

This is where lifetime wealth planning shines. By considering your entire financial picture, you can make more strategic decisions, balance your short- and long-term goals, and maximize the likelihood of achieving financial security. It also gives you the flexibility to adjust your plan as life changes—whether through a career transition, a significant purchase, or the need to reassess your investment strategies.

Key Components of Lifetime Wealth Planning

- Goal Setting and Prioritization

- Step 1 in lifetime wealth planning is setting clear financial goals. These goals can vary based on life stage: saving for a home in your 30s, investing for growth in your 40s, planning for retirement in your 50s, and focusing on wealth preservation or estate planning in your 60s and beyond. Defining these goals allows you to set a financial course with purpose and direction.

- It is equally important to prioritize these goals. Should you pay off debt first or invest more aggressively? Should you save more for your child’s education or focus on retirement? Lifetime wealth planning helps you balance these competing priorities over time.

- Holistic Financial Management

- Unlike ad hoc financial planning, lifetime wealth planning covers every facet of your finances. This means considering cash flow management, debt management, tax strategies, investments, retirement savings, and estate planning as part of a cohesive plan.

- This process is critical to understanding how your income and expenses fit your goals. Monitoring your cash flow—what you earn versus what you spend—is foundational for determining how much you can save and invest.

- Investment Strategy

- Investing plays a significant role in building wealth over a lifetime. However, your strategy in your 30s should differ from those in your 50s or 70s. Lifetime wealth planning involves adjusting your asset/liability allocation as you move through different life stages.

- At any time in the future, asset/liability decisions are determined based on your unique circumstances. Rules of thumb are not sufficient for everyone. For example, systematically lowering risk as you approach retirement may sound sensible for those that have little wealth available for their retirement years and are very risk averse to any losses. Someone else that has more than enough to retire on, may want a strategy with higher expected return and risk because they are managing this money for their heirs with a much longer horizon than their own. It’s all about you. Risk Management

- No wealth-building plan is complete without a way to manage risks. Risk management includes not just investment risk but also insuring yourself against life’s worst outcomes—whether through health, life, homeowner’s, or auto insurance or disability coverage. These safety nets provide for offsets to downside outcomes from unlikely events due to illness, sudden death, damage to a large asset (home) or job loss that creates the need for a reevaluation of lifetime planning.

- In addition, the farther away from now, the more risk there is to be expected. Imagine all the downside and upside events that can occur over the next month compared to what can happen over the next 30 years. Risk expands with time. Hence, a variety of expected future net worth versus risk paths needs to be available to choose from as part of lifetime wealth planning. Each path will have a different value for downside risk when a user sees the probability of running out of money before retirement as well as before the end of retirement. This part of the process allows the user to select their preferred lifetime expected reward versus risk strategy for attaining their goals based on what the market for securities is currently offering.

- Tax Efficiency

- Taxes can significantly reduce your wealth accumulation if not managed properly. Lifetime wealth planning incorporates tax-efficient strategies for your investments and retirement savings. This can include choosing tax-deferred accounts like IRAs or 401(k)s, leveraging capital gains, or optimizing withdrawals in retirement to minimize your tax liabilities.

- Estate planning is another important aspect of tax management. Planning can reduce the tax burden on your heirs and ensure that your assets are transferred efficiently.

- Estate Planning

- Planning to transfer your assets after death is often overlooked in wealth management, but it’s crucial for leaving a lasting legacy. Estate planning involves more than just writing a will—it requires strategic thinking about preserving and distributing your wealth, minimizing taxes, and providing for your loved ones. Consider including bequest in your lifetime wealth plan.

- Whether through trusts, charitable donations, or other vehicles, estate planning should be done with your lifetime wealth plan to protect your financial legacy.

Benefits of Lifetime Wealth Planning

- Long-Term Security

- The primary benefit of lifetime wealth planning is long-term financial security. By carefully mapping out your goals and creating a strategy to meet them, you can build a foundation that supports your lifestyle and provides peace of mind for the future.

- Flexibility

- Life rarely goes according to plan. Whether it’s a job change, market fluctuations, or unexpected expenses, your financial strategy must be flexible enough to adapt. Lifetime wealth planning allows that flexibility, providing the tools to adjust as your life and goals change.

- Peace of Mind

- Knowing that you have a comprehensive plan for the future can alleviate much of the stress of managing your finances. With a clear path forward, you can make decisions confidently, knowing you’re prepared for the expected and the unexpected.

- Holistic Approach

- Because lifetime wealth planning considers all aspects of your financial life, you avoid the pitfalls of focusing too much on one area at the expense of another. This holistic approach ensures that your short-term actions support your long-term goals.

How WealthFluent Simplifies Lifetime Wealth Planning

WealthFluent’s platform is designed to take the complexity out of lifetime wealth planning by providing all the tools you need in one place. With WealthFluent, you can:

- Set and track your financial goals, adjusting them as life changes.

- Monitor your cash flow, expenses, and savings to ensure you build wealth efficiently.

- Create and manage a comprehensive investment strategy that dynamically adapts to every stage of your life.

By integrating all aspects of your financial life into a single, streamlined interface, WealthFluent makes building, managing, and protecting your wealth for the long term easier than ever.

Conclusion: A Blueprint for Financial Success

Lifetime wealth planning is not just about managing your money today—it’s about building a long-term strategy that adapts to your life and helps you achieve financial freedom. With the right plan, you can make informed decisions, mitigate risks, and secure your financial future.

WealthFluent is here to support you every step of the way. Our platform offers the tools and guidance you need to create a customized wealth plan that evolves with you. Whether you’re just starting out, middle aged, nearing retirement or in retirement, lifetime wealth planning is the key to building a financially secure life.

Be on the lookout for our next blog post, where we will discuss best practices for portfolio management and optimization—the real tool you need to keep you on track to retire the way you want.